Digital services exports continue to serve as a key driver of broader gains for the U.S. economy. The latest data released by the U.S. Department of Commerce on July 3 illustrates how digital trade continues to increase year-over-year, generating a hefty surplus and bolstering U.S. services trade overall.

In 2023, U.S. exports in digitally deliverable services generated $655.5 billion, up from $637 billion the year prior, according to the latest data released from Commerce’s Bureau of Economic Analysis. Meanwhile, the trade surplus in digitally deliverable services increased to $266.8 billion more exports than imports in 2023. That number was $254.5 billion in 2022. Digitally deliverable services exports represented 64% of all U.S. services exports in 2023, a key area of strength in overall trade for the United States.

As detailed by a recent post from the Council of Economic Advisers (CEA) that I previously covered, “the services trade surplus has been fueled primarily by the growth in digitally-enabled services” since the late 2000s and the “growth in U.S. digitally-enabled services exports has far outpaced the growth in exports of other services as well as exports of goods over the last 25 years.” CEA noted that the trend “comports with the expansion of the U.S. digital economy” and further highlighted how, in 2022, “while U.S. real GDP grew by 1.9 percent, the U.S. digital economy real value added grew by 6.3 percent driven primarily by growth in software and telecommunication services.” Meanwhile, the President’s Export Council released a set of recommendations in line with this narrative the same week, arguing that the Administration should “re-establish U.S. leadership on digital services trade globally” to protect the “virtuous cycle (success of service exports overseas and job growth at home) [that] is increasingly at risk by the ongoing rise of market access restrictions and discriminatory rules targeting digital services in markets around the world.”

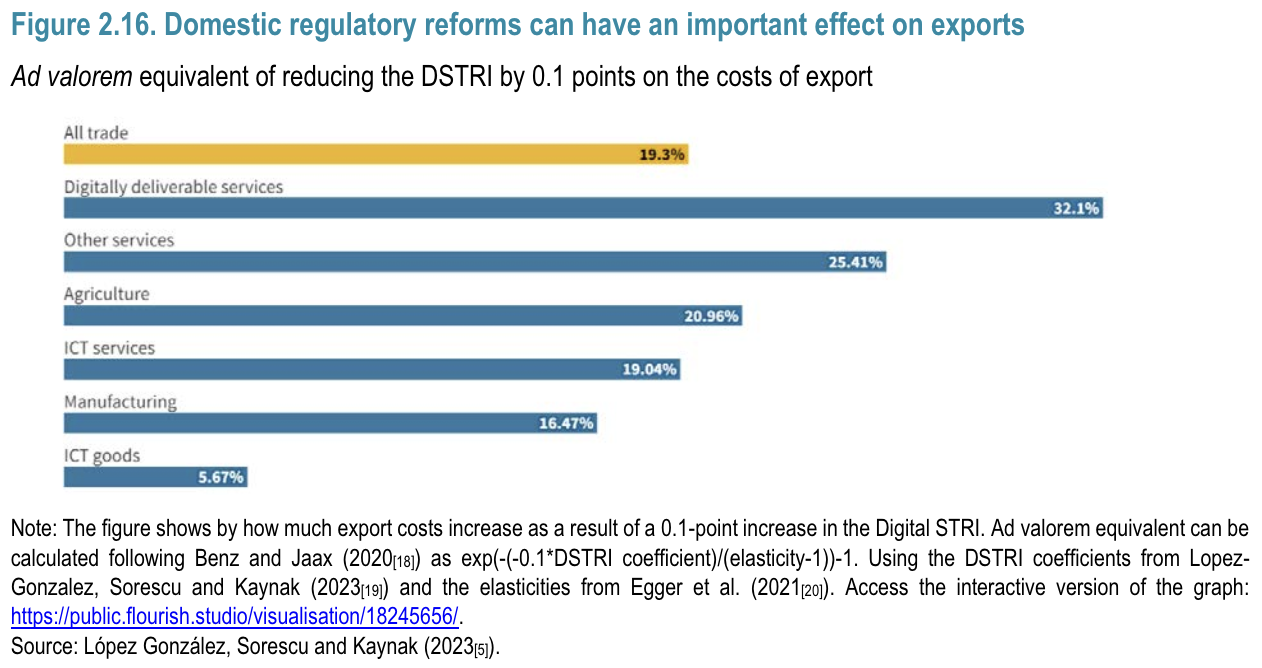

This continued boom in digital services exports is all the more notable given the proliferation of barriers to entry to global markets. According to a recent report from the OECD, barriers to digitally-enabled services increased by 25% globally between 2014 and 2023, a trend “driven by increasing regulatory hurdles that affected communication infrastructures and data connectivity.” The OECD also found that reducing digital barriers—based on an OECD scale known as Digital Services Trade Restrictiveness Index (DSTRI)—dramatically decreases the costs of trade overall.

Source: OECD

Europe offers an interesting vignette into this phenomenon. The European Union is a major market for the United States in services and digital services specifically. U.S. exports of services to the EU generated $261.7 billion in 2023, and the U.S. trade surplus in services with the EU was $71.2 billion in 2022, the most recent year with available data.

However, Europe has adopted an increasingly aggressive agenda in pursuit of “digital sovereignty” that has undermined U.S. firms’ operations in the bloc. Marquée legislation such as the Digital Markets Act and subsequent restrictions stemming from the law, as well as more opaque and traditional protectionist policies such as France’s cloud restrictions through its SecNumCloud policy (being considered as part of the EU Cloud Cybersecurity Certification Scheme) are two key examples of this trend.

Looking at the data for U.S. exports in information and communications technology services—a narrower category of digital services than “digitally-enabled services,” but one for which data is available for every region for the past four years—the effects of the EU’s efforts become clear. While U.S. exports in ICT services to the EU grew 13% between 2020 and 2023, the same exports grew in the same time period by 18% to the Asia-Pacific, 20% to the Americas, and 21% to Africa and the Middle East. If narrowed to year-over-year, U.S. ICT services exports to the EU—a 3% gain between 2022 and 2023—still trailed behind those to the Americas (9%) and Africa and the Middle East (13%). Some European policymakers have begun to realize these costs, calling for less restrictive, fairer regulations, to ensure that the bloc continues to benefit from access to high quality foreign goods, services, and investments.

Of course, the volume of digital services exports to Europe remains high and is increasing, and it is important to note that there is also a growing list of barriers to digital firms’ operations globally, particularly in the Asia-Pacific where countries are influenced by China’s approach to governance. However, as the United States government reviews the impact of the EU’s laws and regulations, it must ensure these efforts are not duplicated in other key markets where exports continue to grow at higher rates than in the EU.

Addressing digital barriers is important to continuing to nurture digital exports’ impact on the U.S. economy as well as broader diplomatic goals of combating the expansion of China and Russia’s view of digital governance. The data released by the BEA is a timely reminder of what is at stake and the need to promote digital solidarity and tackle the spread of digital trade obstacles around the world.